You've seen that three-digit number before, but did you know it tells a story? It's essential to understand this magic number in order to preserve or improve your credit, as it can directly impact your financial health.

What is a Credit Score and Why is it Important?

A credit score is an indicator of a person's creditworthiness, indicating their ability to repay debts. It's a reference for lenders when they're determining your ability to acquire a loan, receive insurance, buy a house, lease a car, rent an apartment, or even get a job. A good credit score can open doors, while a bad one may cost you money.

What is a Good Credit Score?

The three largest nationwide credit bureaus are Equifax, TransUnion, and Experian. Each one may contain different information on file about you, so your credit score may differ across all three by a few points. While there are several different credit-scoring models, financial institutions mostly use the FICO Score. According to the FICO Score, credit scores range from 300 to 850 and the following tiers are used:

- Exceptional (800+): A credit score in this tier tells lenders you are especially low risk as a borrower.

- Very Good (740 to 799): A very good credit score is above average and tells lenders you are low risk as a borrower.

- Good (670 to 739): According to Experian, the average FICO Score in the U.S. was 714 in 2022, unchanged from 2021. Most lenders consider this a good score.

- Fair (580 to 669): This tier contains below-average scores showing lenders you present a certain level of risk. However, you can still get approved for loans and credit cards with a credit score in this range.

- Poor (579 or below): This credit score is well below the U.S. average and tells lenders you may be a risk.

Factors that Affect a Credit Score

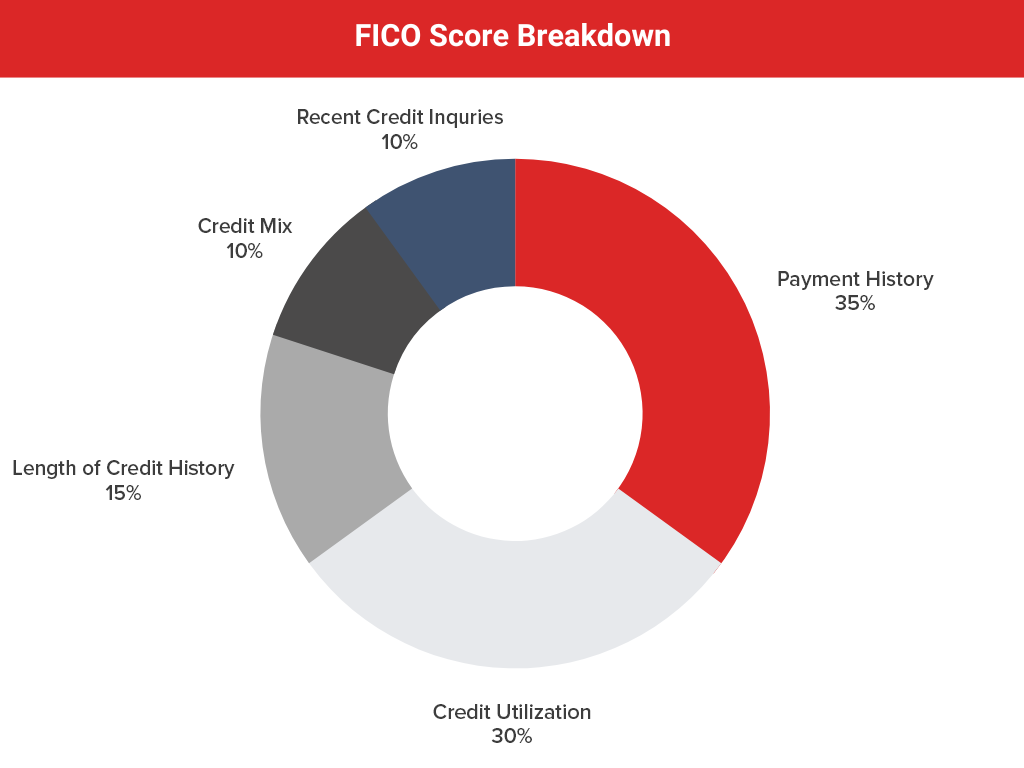

You can improve your credit over time by understanding how your credit score is determined. When it comes to your FICO Score, these are the factors that affect it:

Payment history is one of the most critical factors making up 35% of a person's credit score. Late payments, defaults, or missed payments can negatively impact the score. Lenders consider this a red flag because it indicates a person cannot repay debts on time.

Credit Utilization is the second most crucial factor that affects a credit score. High credit card or loan balances can indicate that a person may struggle to manage their finances. There is no concrete number, but a good rule of thumb is to keep your credit utilization below 30%. Keeping credit card balances low and paying off debts on time is essential to improve credit scores and builds good financial habits.

Length of credit history is also an essential factor. An extended credit history provides more information and tells a better story for lenders to determine a person's creditworthiness. Therefore, it is important to establish credit as soon as possible and maintain a long history of responsible credit use.

New credit applications can impact the score as well. When you submit a credit application, your credit score gets a "hard inquiry," which can cause a temporary drop in your score. In addition, applying for multiple new credit lines in a short period can also impact your score and raise a red flag for lenders.

Credit mix is the final factor credit bureaus pay attention to and is defined as the mix of different types of credit you have. This includes revolving credit accounts, retail accounts, or installment loans. Having a "mix" of accounts in good standing can help tell the story of your creditworthiness.

Tips for Maintaining and Improving Your Credit Score

To keep your credit score in good shape, you'll want to use any credit you have responsibly. Here are several steps you can take to improve your score:

- Pay your bills on time. This is essential to maintaining a good credit score because it makes up most of your FICO Score. Setting up automatic payments or reminders can help ensure timely payments.

- Keep credit card balances low. Keeping your credit utilization at or below 30% of the credit limit will generally help your score. Simply put, having a balance of $3,000 or less for a credit card with a limit of $10,000 demonstrates that you are financially responsible. Paying off debts can also help improve credit scores.

- Maintain long credit history. Keeping old credit accounts open is crucial, even if they are not used regularly. Closing old accounts can shorten a person's credit history and lower their credit score.

- Limit new credit applications. Only applying for new credit when necessary and avoiding applying for multiple new credit lines in a short period can help maintain a good credit score.

- Monitor your credit reports. Keep a close eye on your credit report for accuracy, and make sure you report any errors you may find.

In conclusion, credit scores are essential for determining a person's creditworthiness, and as we've learned, several factors impact the score. Paying bills on time, keeping your credit balances low, maintaining a long credit history, limiting new credit applications, and monitoring your credit reports give you the power to maintain or improve your credit score over time.

Tags: credit cards, credit score, personal finance,