What is an IRA?

IRAs are tax-advantaged investment accounts designed to help you prepare for retirement. IRAs can be a good tool for individuals who are self-employed, don’t have access to an employer-based retirement plan, or who are already contributing the maximum to their employer-based plan.

Essentially, an IRA allows you to contribute money to your retirement savings and you get to choose how your money is invested. “Tax-advantaged” means that depending on the type of IRA you choose, you’ll either pay no taxes when you put money in or when you take money out.

How do they work?

With an IRA, the funds that you contribute can be invested in many different types of assets, such as CDs, Money Market Accounts, stocks, bonds, etc. You can choose how your funds will be invested, according to your goals and risk tolerance. Additionally, you have the option to adjust your asset allocation, moving funds from one investment type to another without incurring capital gains taxes.

However, because an IRA is designed for retirement savings, you’ll have to leave your money in there until you are of retirement age. Withdrawals from an IRA before you are 59 ½ are subject to taxes plus a 10% penalty. There are a few exceptions that allow you to use IRA funds without incurring penalties, such as buying your first home or paying for college, but there are extra rules governing each of these situations. Consult with your tax professional or a financial advisor to make sure you understand the implications before using IRA funds for special exceptions.

There are limits to the amount you can contribute each year to an IRA. Individuals age 49 and younger can contribute up to $6,500 per year, while those who are 50 – 70 ½ years old can contribute up to $7,500 per year. This applies across all traditional and Roth IRAs owned by an individual, not per account. If you have more than one IRA, your total contributions across all your accounts cannot exceed the annual contribution limit.

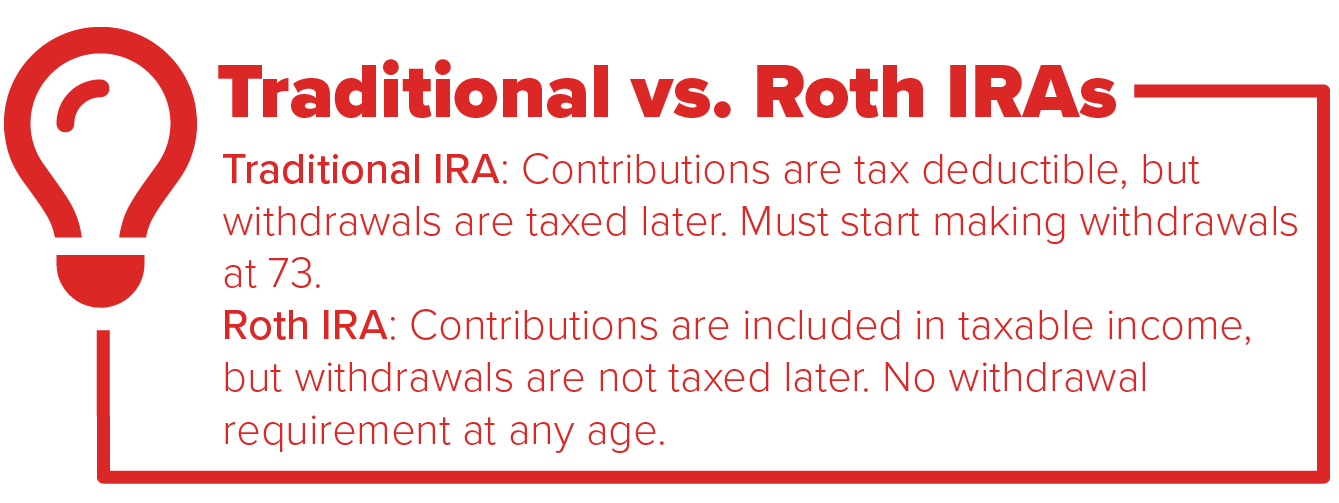

Types of IRAs

There are two types of IRAs available: traditional and Roth. The main differences between them are when you pay taxes and if you are required to withdraw funds.

Traditional IRAs

The contributions you make to a traditional IRA are typically tax-deductible in the year you make the contribution. However, when you withdraw the funds later, you’ll pay taxes on the full amount that you withdraw. You must start making withdrawals called Required Minimum Distributions once you turn 73 years old.

Traditional IRAs are good for people who are looking for tax deductions now or who expect to be in a lower tax bracket when they retire.

Roth IRAs

Contributions made to a Roth IRA are not tax-deductible. You’ll pay income taxes now, but the withdrawals you make in retirement will not be taxed. Additionally, there is never any requirement to make withdrawals from a Roth IRA.

Roth IRAs are good for people who are expecting to earn more at retirement or who are a long way from retirement.

How do I choose?

While it is important to think about your current tax status versus your taxes in retirement, it is really difficult to predict what your tax situation will be like very far into the future, especially if you are younger or a long way from retirement. It is important to think about the other sources of income you plan to have in retirement and consider how you can diversify your tax exposure. For example, if you have a 401(k) that you plan to use as retirement income, you’ll be paying taxes on those distributions. Social Security Benefits are also taxable income for most individuals. Choosing a Roth IRA and paying taxes now could give you another source of retirement income that does not result in a higher tax bill. As always, when considering any financial decision that may affect your tax status, it is a good idea to consult with your tax professional.

Eligibility and Limitations

To open an IRA, you or your spouse must have earned income from a job. There are some additional IRS requirements to take advantage of the tax breaks. If you participate in an employer-based retirement plan, such as a 401(k), Traditional IRAs have limits on tax deductions based on your income and filing status . In addition to the general contribution limit, Roth IRAs have limits governing how much you can contribute (if at all), depending on your income and filing status. Check the IRS’s updated contribution limits and deduction requirements to make sure that you are eligible and can get all of the benefits of an IRA.

Opening and moving IRAs

You can open an IRA at many different types of institutions within the financial services industry, such as banks, credit unions, brokerage firms, etc. When comparing your options, be sure to pay attention to monthly fees, commissions, and minimum opening requirements, as these are set by each company. Farm Bureau Bank offers a variety of IRA options with no monthly fees.

Do you have an old retirement account from a former employer? If you already have an IRA or 401(k) but would like to move it to another company, there are a few ways you can do this to avoid taxes and penalties.

Conclusion

Whether you’re just starting out on your retirement savings journey, looking for tax deductions, or you’re planning to diversify your retirement income and tax exposure, an IRA can be a valuable tool in your financial kit. The flexibility of choosing how your contributions are invested, plus the up-front or down-the-road tax break allows you to take charge of your future however you choose.

Tags: personal finance, savings